Buying the dip has once again worked (for now). This has invigorated stock investors as we've seen money pouring back into stocks the past two weeks. At the same time, bond investors are running for the exits leading to the question of, who is right? Who do you want to place your bets with – bond traders or stock traders? One is right, one is wrong. Picking the wrong side could have severe consequences on your financial plan.

Weekly Talking Points

- Even if the conflict in Ukraine ends quickly, we are back to where we were at to start the year – stocks are overvalued, economic growth is slowing, inflation is borderline out-of-control, and the Federal Reserve will be raising rates and pulling back stimulus.

- There are still more scenarios for additional risks than additional rosy scenarios for the stock market.

- The bond market is saying the Federal Reserve is way behind the inflation curve and is raising rates for them at a furious rate. Consumer sentiment is saying inflation is taking a huge bite out of future spending plans. Stocks are saying there is no risk in the market.

- If you were overweight stocks going into the year, any bounce should be looked at as a selling opportunity. We're well overdue for a real bear market.

- SEM's allocations are close to minimum exposure across the board. Unless your financial plan, cash flow strategy, or investment objectives have changed, there is no need for action on your part.

I don't have a lot to say/add to the talking points above. It is fascinating to look at where stocks are at versus bonds. Remember back in January when the Fed hinted they would be raising rates about 6 or 7 times in 2022? The stock market had already begun to sell-off the first week of January when several Federal Reserve members said the same thing. The selling continued after that January meeting. This week the Fed still said to expect 6 or 7 rate hikes, but apparently stock investors/traders/speculators took solace that the Fed Chair seemed to care more about the economy than inflation getting out of control.

The stock market is now basically where it was after the January meeting.

The bond market on the other hand, is saying inflation is a problem and the Fed has been and continues to be way too slow in raising rates. They've done it for them.

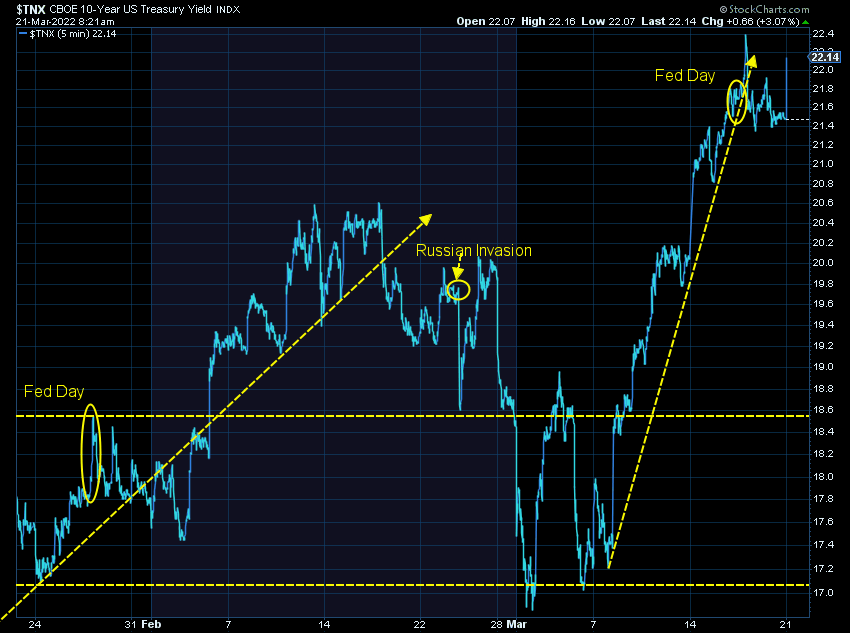

Here are 10-year yields. Yields were at 1.6% when the year started. The free market has hiked long-term rates by 0.6% in less than 3 months. Keep in mind, if the market trusted the Fed to rein in inflation, we would see short-term rates rising and long-term rates declining or at least stabilizing. Inflation erodes the value of dividend payments. If it is thought to be a short-term phenomenon, long-term rates would be stable.

This is hurting the bond market overall. Here's a look at the Aggregate Bond Index ETF. As investors have learned, sometimes stocks and bonds go down in value at the same time. It hasn't happened much the past 30 years, but we also haven't had inflation this high in the past 30 years.

I've always said, "bond traders are much smarter than stock traders in terms of economic expectations. Bond traders care about actually getting their money back. Stock traders only care about being able to sell at a higher price. When bond traders are worried, I'm worried."

I've been a long critic of the Federal Reserve. Their focus on keeping stock markets high at the risk of creating asset bubbles has done far more harm than good. They've created a stock bubble once again by keeping their foot on the gas pedal following the last stimulus bill a little over a year ago. It is unfathomable to me that they not only kept interest rates after Congress dumped 25% of GDP into the economy, but they also kept creating money every single week for the past two years.

I shared this quote and chart last week. It's what I said a year ago. In case you missed it, here's a link to last week's much longer article.

The sad part is this bill will end up hurting the lower half of our economy more over the long run. Throwing money to people who didn't need it will create inflation, cause interest rates to go up, and ultimately hurt job growth. I'm predicting a recession in late 2022 or early 2023 when this temporary boost is no longer there and we're left with the unstable economy we had at the beginning of 2020.

With that, I'm going to call it a week. Our systems are still "bearish", but if the market rally broadens out we could easily flip back to a more "neutral" or even "bullish" position. For now, it looks like this was an overdue (and possibly overextended) bounce. Regardless, my opinion doesn't factor in to how we manage money.